Financing an electric bike can seem like a convenient way to get your hands on the latest model without breaking the bank upfront.

With many retailers offering attractive financing options, it’s easy to see why so many people might be tempted.

However, financing an electric bike can often lead to a series of financial pitfalls that outweigh the immediate benefits.

From high interest rates to hidden fees, the seemingly small monthly payments can quickly add up.

6 MAIN Reasons Why Financing An E-bike Is Bad

High-Interest Rates

One of the most significant drawbacks of financing an electric bike is the high interest rates that often accompany these deals.

Interest rates can be steep, sometimes reaching as high as 20% or more, depending on your credit score and the financing company.

This means that by the time you finish paying off the loan, you may have paid a considerable amount more than the original price of the bike.

For example, if you finance a $2,000 electric bike at a 20% interest rate over 36 months, you will end up paying over $2,500 in total.

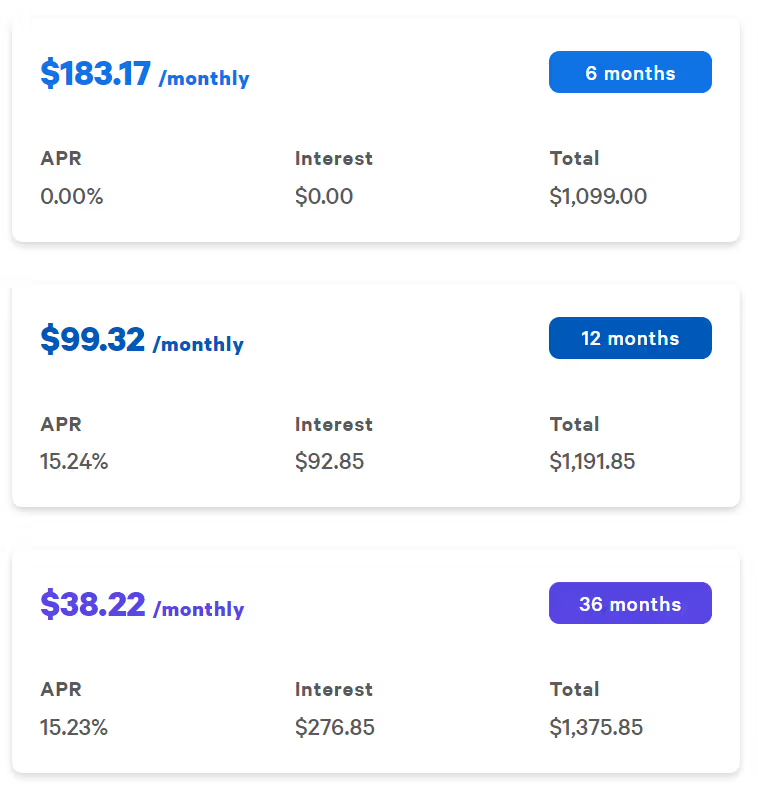

In our screenshot below, we will take an example of purchasing an e-bike from Rad Power via Affirm Financing.

If the original buying price for that e-bike is $1099, you will end up paying $1375 in 36 months.

Depreciation

Electric bikes, like cars, depreciate in value over time. As new models and technologies emerge, your electric bike will lose value quickly.

When you finance a bike, you’re committing to paying its original price over a period, even as its market value declines.

Should you decide to sell or trade in the bike later, you may find that it’s worth significantly less than the amount you still owe.

This depreciation can result in negative equity, where you owe more than the bike is worth, making it difficult to sell without incurring a loss.

When e-bikes or other electric rides are outdated for that matter, you will be lucky to get half of the buying price or any offer for that matter.

Long-term Financial Commitment

Financing a bike locks you into a long-term financial commitment, which can be burdensome, especially if your financial situation changes unexpectedly.

A job loss, medical emergency, or any unforeseen expense can make it challenging to keep up with the monthly payments.

Falling behind on payments can lead to penalties, damaged credit scores, and potential repossession of the bike. Unlike paying in cash, which offers the flexibility to adjust your spending based on current financial conditions, financing ties you to a rigid payment schedule.

Hidden Fees and Charges

Many financing agreements come with hidden fees and charges that are not always transparent at the time of purchase.

These can include origination fees, prepayment penalties, and late payment fees. Origination fees are often charged by lenders to process the loan, while prepayment penalties can prevent you from paying off your loan early without incurring additional costs.

Such charges can significantly increase the total cost of the bike beyond the advertised price, catching consumers off guard.

Limited Value Addition

While financing might allow you to ride a high-end electric bike today, it’s essential to consider whether the additional features justify the added cost.

Many financed bikes come with unnecessary features that inflate the price but offer little practical value. When paying in cash, you’re more likely to prioritize essential features, ensuring you get the best value for your money.

Psychological Impact of Debt

Lastly, the psychological impact of carrying debt should not be underestimated. Being in debt can create stress and anxiety, particularly if you struggle to make payments. This financial strain can affect your overall quality of life and negate the enjoyment of owning an electric bike.

Better Alternatives

Instead of financing an electric bike, consider exploring other options.

Saving up and paying cash is the most straightforward approach, allowing you to avoid interest and fees altogether.

Buying a second-hand electric bike is another viable option, offering significant savings while still providing the benefits of electric mobility. Many sellers offer gently used models at a fraction of the cost of new ones. You can find such sellers on Online Marketplaces and sites such as Upway.

Additionally, renting an electric bike for occasional use or subscribing to a bike-sharing service can be more cost-effective for those who do not ride regularly.

In Summary

Financing an electric bike might offer immediate gratification, but it often comes with a slew of financial drawbacks.

High interest rates, hidden fees, depreciation, and long-term financial commitments can make financing an unfavorable option.

By considering alternatives such as saving up, buying second-hand, or renting, you can enjoy the benefits of electric biking without the burden of debt.

Making an informed and financially sound decision ensures that you can ride your electric bike with peace of mind, knowing it’s truly yours without the strings attached.